Unlocking Your Home’s Potential: Why 2026 is the Year to Strategize

For homeowners in the DC, Maryland, and Virginia (DMV) region, the real estate market has been a powerful engine for wealth creation. As we navigate 2026, many property owners are sitting on a substantial amount of untapped home equity. However, simply having equity is not enough. The most successful homeowners are leveraging their property’s value to build long-term wealth, upgrade their living spaces, and secure their financial futures.

A well-planned cash-out refinance can be a transformative financial tool. Whether your goal is to consolidate high-interest debt, fund a major home renovation, or purchase an investment property, having a sophisticated strategy is key. At The Mortgage Know, we believe in providing consultative, client-first advice. With over 25 years of mortgage industry experience, independent broker Richard Jones is dedicated to helping DMV residents make confident mortgage decisions tailored to their unique financial landscapes.

High-Return Renovation and Debt Consolidation Tactics

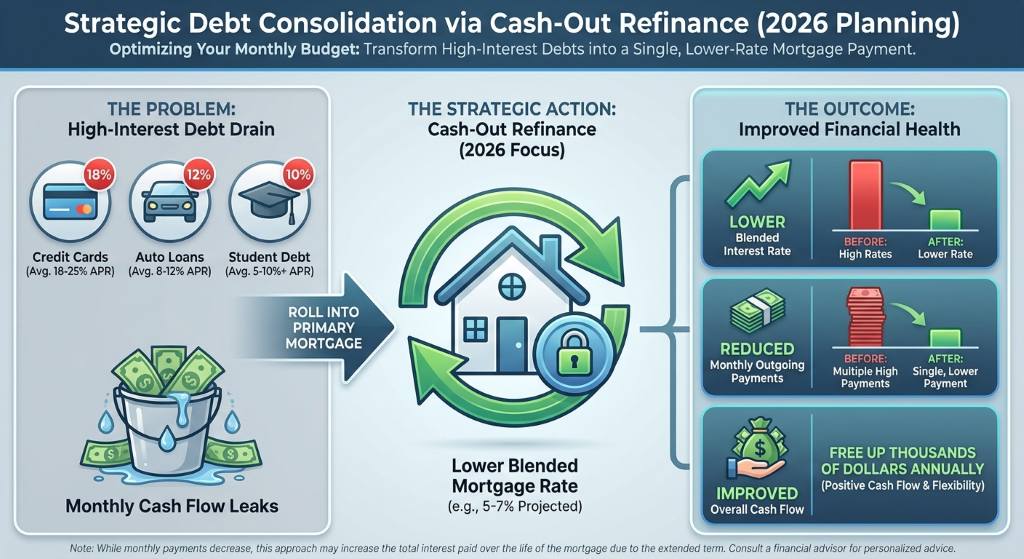

One of the smartest ways to utilize a cash-out refinance in 2026 is through strategic debt consolidation. Credit card interest rates and personal loan costs can drain your monthly budget. By rolling high-interest debts into your primary mortgage, you can significantly lower your blended interest rate, reduce your monthly outgoing payments, and improve your overall cash flow.

- Debt Consolidation: Pay off credit cards, auto loans, or student debt to free up thousands of dollars annually.

- Home Renovations: Reinvest in your current property. Upgrading kitchens, bathrooms, or adding an accessory dwelling unit (ADU) can dramatically increase your home’s resale value in the competitive DMV market.

- Flexible Financing: As an independent mortgage broker, we offer access to diverse loan programs, ensuring you get the most competitive rates available.

When you work with an expert like Rich Jones, we analyze your financial situation to explore multiple loan options. We clearly explain the benefits and requirements of each path so you can choose the strategy that aligns perfectly with your goals.

| Debt Type | Current Balance | Average Interest Rate | Current Monthly Payment | Estimated Payment After Refinance |

|---|---|---|---|---|

| Credit Cards | $25,000 | 22.5% | $750 | Included in Mortgage |

| Auto Loan | $30,000 | 8.5% | $650 | Included in Mortgage |

| Personal Loan | $15,000 | 11.0% | $400 | Included in Mortgage |

| Total | $70,000 | N/A | $1,800 | ~$450 (Added to Mortgage) |

Building Long-Term Wealth with Your Home Equity

Beyond debt reduction and home improvements, your home equity can serve as the foundation for generational wealth. Many savvy DMV homeowners are using cash-out refinances to secure down payments for investment properties. With specialized products like DSCR (Debt Service Coverage Ratio) loans, you can qualify for an investment property based on the rental income it generates rather than your personal income.

This sophisticated approach allows you to diversify your portfolio and create passive income streams. Whether you are a first-time investor or an experienced landlord, having a trusted advisor is crucial. We handle the application, documentation, and lender coordination to keep everything moving smoothly toward closing.

Ready to explore your options? Learn more about our independent broker access and how we prioritize your best interests. Compliance Note: Rich Jones is a Licensed Mortgage Advisor (NMLS #1192902) with The Loan Advisors, LLC. All loans are subject to credit approval and program guidelines.

Q1: What is a cash-out refinance and how does it work for DMV homeowners?

A cash-out refinance replaces your current mortgage with a new, larger loan. You receive the difference between the two loans in cash. DMV homeowners often use this strategy to access their accumulated home equity for renovations, investments, or debt consolidation.

Q2: Can I use my home equity to buy an investment property?

Yes. Many homeowners use the funds from a cash-out refinance as a down payment for a second home or an investment property. We offer specialized loan programs, including DSCR loans, to help real estate investors grow their portfolios.

Q3: Is debt consolidation through a mortgage refinance a smart financial move?

It can be highly beneficial. By paying off high-interest credit cards or personal loans with a lower-interest mortgage, you can significantly reduce your total monthly payments and save money on interest over time. We can help you run the numbers to ensure it makes sense for your specific situation.

Q4: Do I need perfect credit to qualify for a cash-out refinance in 2026?

Not at all. While higher credit scores often secure the best rates, there are many flexible loan programs available for borrowers with varying credit profiles. We will review your financial picture and explore the best options for you.

Q5: How do I know if I have enough equity in my home to refinance?

Generally, lenders require you to maintain at least 20 percent equity in your home after a cash-out refinance. We can help you estimate your home’s current market value and calculate your available equity during a free consultation.Schedule Your Free Mortgage Consultation Today