Insider Moves on IRRRL Timing and Entitlement Restoration in the DMV

As we look toward the 2026 housing market in the Washington D.C., Maryland, and Virginia (DMV) region, veterans and active-duty military members have unique opportunities to maximize their housing benefits. Standard lenders often overlook advanced VA loan strategies that can save you thousands. At The Mortgage Know, Richard Jones utilizes over 25 years of experience to uncover strategies that maximize your benefits.

One of the most powerful tools available is the VA Interest Rate Reduction Refinance Loan (IRRRL). However, timing is everything. Many homeowners rush into a refinance without understanding the strict seasoning requirements or the net tangible benefit rules. To properly execute an IRRRL strategy in 2026, you must consider the following:

- Seasoning Requirements: You must wait at least 210 days from the date of your first payment on the original loan before closing on an IRRRL.

- Net Tangible Benefit: The VA requires that your new interest rate is substantially lower, ensuring the refinance actually saves you money.

- Market Timing: Tracking DMV market fluctuations allows you to lock in a rate exactly when local bond markets dip.

Beyond refinancing, entitlement restoration is a critical strategy for military members PCSing out of the DMV or upgrading their local home. Many veterans do not realize they can fully restore their VA entitlement. If you sell your current VA-financed home, you can restore your entitlement for your next purchase. Alternatively, you might use second-tier entitlement to keep your current home as a wealth-building rental property while buying a new primary residence.

Residual Income Optimization and Local DMV Incentives

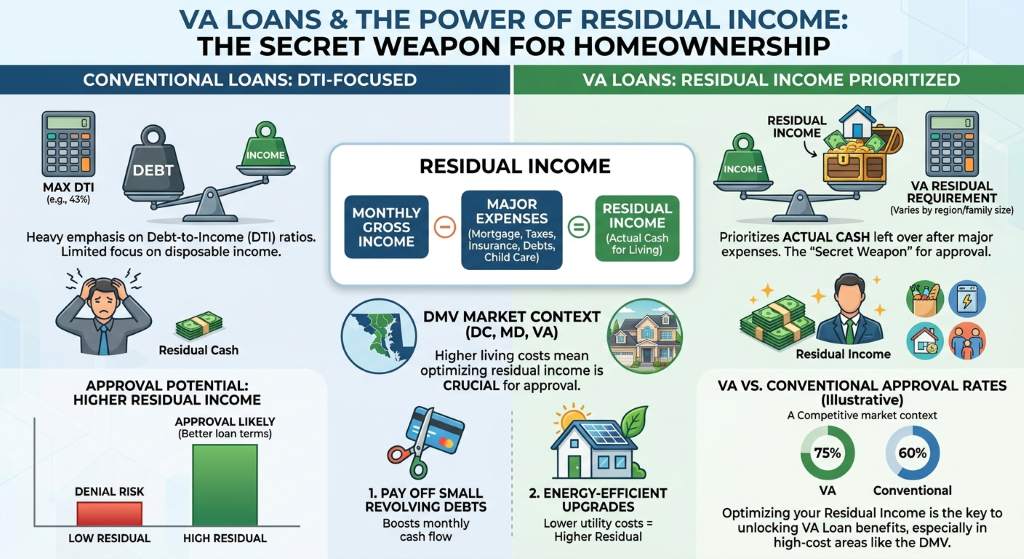

Residual income is the secret weapon of the VA loan program. While conventional loans focus heavily on Debt-to-Income (DTI) ratios, VA loans prioritize residual income. This is the actual cash left over each month after major expenses are paid. In the higher-cost DMV market, optimizing your residual income can be the difference between an approval and a denial.

To optimize your residual income, consider paying off small revolving debts before applying, or structuring your loan to include energy-efficient improvements that reduce estimated monthly utility costs. Furthermore, local incentives make a massive difference. Maryland, Virginia, and Washington D.C. offer incredible property tax exemptions for disabled veterans. Combining these exemptions with your VA loan can significantly increase your purchasing power by removing hefty property taxes from your monthly housing expense.

If you are exploring loan programs, understanding how these local tax incentives interact with VA residual income guidelines is essential for a smooth approval process.

| Family Size | Northeast Region (Includes MD/DC) Minimum | South Region (Includes VA) Minimum | Strategy Impact |

|---|---|---|---|

| 1 | $450 | $441 | Easily met with local tax exemptions. |

| 2 | $755 | $738 | Debt consolidation improves margins. |

| 3 | $909 | $889 | Energy efficiency credits reduce utility estimates. |

| 4 | $1,025 | $1,003 | Requires careful DTI and residual balancing. |

Navigating the DMV Real Estate Market with Expert Guidance

Securing a home in the competitive DMV market requires a lender who understands both the local real estate landscape and the nuances of VA financing. Richard Jones at The Loan Advisors, LLC (NMLS #1192902) operates as an independent mortgage broker. This setup means you get access to wholesale rates and personalized guidance without the hidden fees of big retail banks.

Whether you are a first-time homebuyer, looking to refinance, or wanting to leverage investment loans alongside your VA benefits, expert advice is crucial. We clearly explain each loan option, including benefits, requirements, and potential costs, so you can confidently choose what works best for your financial goals. Discover more about our client-first approach by visiting our About Us page, or take the next step and apply online today.

Q1: Can I have two VA loans at the same time in the DMV?

Yes. Through second-tier entitlement, you can potentially have two VA loans simultaneously if you have remaining entitlement and meet the lender’s income and credit requirements.

Q2: What are the VA loan funding fee rates for 2026?

Funding fees vary based on your down payment and whether it is your first time using the benefit. Veterans with a service-connected disability are typically exempt from paying this fee entirely.

Q3: How does the IRRRL process work for DMV homeowners?

The IRRRL requires less documentation than a standard refinance. You generally do not need a new appraisal or extensive credit underwriting, making it a fast way to lower your rate when market conditions improve.

Q4: Do property tax exemptions affect my VA loan qualification?

Absolutely. If you qualify for a 100 percent disabled veteran property tax exemption in Maryland or Virginia, excluding those taxes from your monthly payment drastically improves your residual income and purchasing power.

Q5: Why should I use an independent mortgage broker for my VA loan?

Independent brokers like Richard Jones are not tied to a single bank. They can shop multiple wholesale lenders to find the most competitive rates and flexible guidelines for your specific financial situation.Schedule Your VA Loan Strategy Session with Richard Jones Today