Navigating Variable Income: Bank Statement Programs and Asset Depletion

Securing a mortgage as a self-employed professional or real estate investor in the DMV (DC, Maryland, Virginia) area can feel like an uphill battle. Traditional lending models often penalize entrepreneurs for maximizing their tax deductions. However, as an independent mortgage broker, The Mortgage Know offers access to specialized alternative underwriting tactics designed specifically for variable income earners.

If your tax returns do not accurately reflect your true purchasing power, bank statement programs provide a highly effective solution. Instead of relying on W-2s or tax returns, lenders evaluate your personal or business bank statements over a 12 to 24-month period to determine your cash flow and qualifying income. This method allows self-employed borrowers to showcase their true financial health.

Another powerful strategy is asset depletion. This underwriting tactic is perfect for high-net-worth individuals who may have lower documented monthly income but possess significant liquid assets. By dividing your total eligible liquid assets by a set term (often 60 to 84 months), lenders can create a qualifying monthly income stream. Key benefits of these programs include:

- Flexibility: Underwriting based on real cash flow rather than taxable income.

- Higher purchasing power: Utilizing your actual business revenue to qualify for larger loan amounts.

- Customized solutions: Tailoring the loan structure to your unique financial footprint.

As a licensed mortgage advisor (NMLS #1192902), Richard Jones has helped countless DMV entrepreneurs leverage these flexible loan programs to secure their dream homes and investment properties.

DSCR Loans and Portfolio Financing for DMV Investors

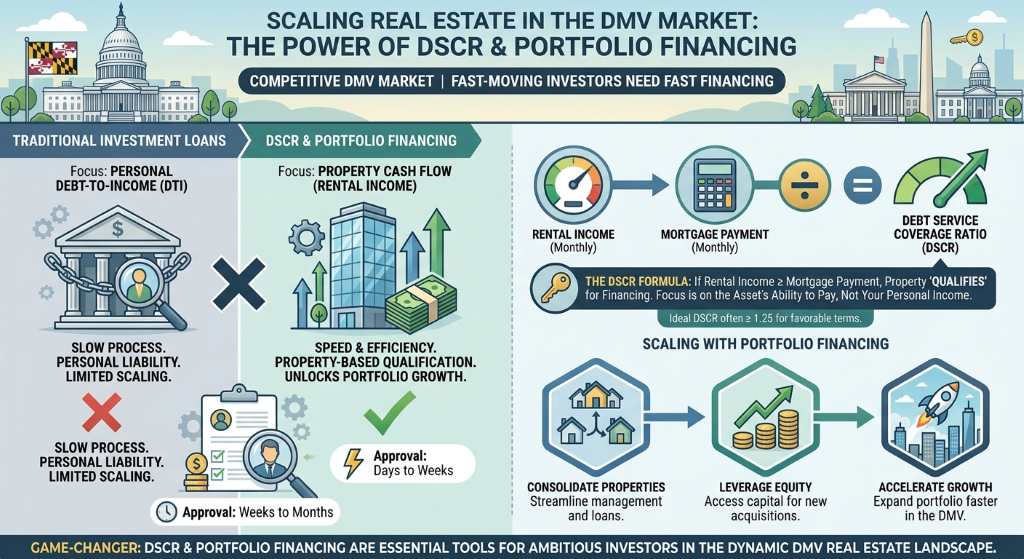

Real estate investors scaling their portfolios in the competitive DMV market require financing that moves as fast as they do. This is where Debt Service Coverage Ratio (DSCR) loans and portfolio financing become game-changers. Unlike traditional investment property loans that scrutinize your personal debt-to-income (DTI) ratio, DSCR loans focus entirely on the cash flow of the property itself.

If the monthly rental income meets or exceeds the monthly mortgage payment, the property essentially qualifies itself. This approach empowers investors to expand their portfolios without being bottlenecked by their personal tax returns. Furthermore, portfolio financing allows investors to bundle multiple properties under a single loan, streamlining management and often reducing closing costs.

When you explore Investment and DSCR Loans, you unlock several strategic advantages:

- No personal income or employment verification required.

- Ability to close in the name of an LLC or corporate entity for added liability protection.

- Unlimited cash-out options to reinvest in new DMV properties.

Working with an independent broker means you have access to a vast network of wholesale lenders, ensuring you receive the most competitive rates and terms available for your investment strategy.

| Loan Program | Best For | Income Verification Method | Key Benefit |

|---|---|---|---|

| Bank Statement Loan | Self-Employed & Freelancers | 12-24 months of business/personal deposits | Bypasses tax returns to show true cash flow |

| Asset Depletion | High-Net-Worth Borrowers & Retirees | Calculation of liquid assets divided by a set term | Converts wealth into qualifying monthly income |

| DSCR Loan | Real Estate Investors | Property rental income vs. mortgage payment | No personal income verification required |

| Portfolio Financing | Investors with multiple properties | Aggregate cash flow of the property portfolio | Consolidates loans and streamlines management |

Expert Strategies for Securing Your Next DMV Property

Preparation is the key to a smooth underwriting process. For self-employed borrowers utilizing bank statement programs, it is crucial to keep business and personal expenses strictly separated. Lenders will analyze your deposits, and commingled funds can complicate the calculation of your qualifying income. Ensure your business accounts reflect consistent, healthy deposits.

For investors eyeing DSCR loans in DC, Maryland, or Virginia, having a solid appraisal and a realistic rent schedule is paramount. The property’s viability is the cornerstone of the loan approval. Partnering with a knowledgeable local expert like Richard Jones at The Loan Advisors, LLC ensures that your application is packaged correctly from day one.

We pride ourselves on transparency, clear communication, and client-first guidance. Because we work for you and not a specific bank, we can navigate the complexities of variable income and alternative lending to find the exact product that aligns with your financial goals. Ready to take the next step? Applying online is quick, secure, and the best way to start exploring your options.

Q1: What is a DSCR loan and how does it work for DMV investors?

A Debt Service Coverage Ratio (DSCR) loan is an investment property mortgage that qualifies borrowers based on the property’s expected rental income rather than their personal income. If the rent covers the monthly mortgage payment, the property qualifies, making it ideal for investors looking to scale quickly.

Q2: Can I get a mortgage in Maryland or Virginia using only my bank statements?

Yes. Bank statement programs allow self-employed borrowers to use 12 to 24 months of personal or business bank deposits to verify income, completely bypassing the need for tax returns or W-2s.

Q3: What does asset depletion mean in mortgage underwriting?

Asset depletion is a method where lenders calculate a monthly qualifying income based on your total liquid assets. This is highly beneficial for high-net-worth individuals, retirees, or entrepreneurs who have significant savings but lower taxable monthly income.

Q4: Do I need perfect credit to qualify for alternative lending programs?

Not necessarily. While higher credit scores can secure better rates, many alternative programs like DSCR and bank statement loans offer flexible credit guidelines. We can evaluate your unique financial picture to find a program that fits.

Q5: How do I start the application process for an investment or self-employed loan?

The easiest way to begin is by scheduling a consultation or completing a secure online application through our website. We will review your goals, analyze your scenario, and present the best mortgage options available.