Navigating the High-Cost DMV Housing Market

Stepping into the real estate market in Washington DC, Maryland, and Virginia can feel overwhelming. The DMV region is known for its competitive, high-cost housing market. However, achieving your dream of homeownership is entirely possible with the right strategy and expert guidance.

As an independent mortgage broker with over 25 years of experience, Richard Jones at The Mortgage Know has helped thousands of buyers secure their ideal homes. For first-time buyers, the secret to competing against cash offers and seasoned investors lies in understanding your loan options and leveraging local resources.

- Understand your purchasing power: Getting pre-approved sets a clear budget and shows sellers you are serious.

- Explore diverse loan types: Do not limit yourself to conventional mortgages when government-backed options might suit you better.

- Work with a local expert: Partner with a broker who knows the nuances of DC, MD, and VA real estate regulations.

By taking a consultative, client-first approach, we ensure you have the tactical advantage needed to succeed in this bustling market.

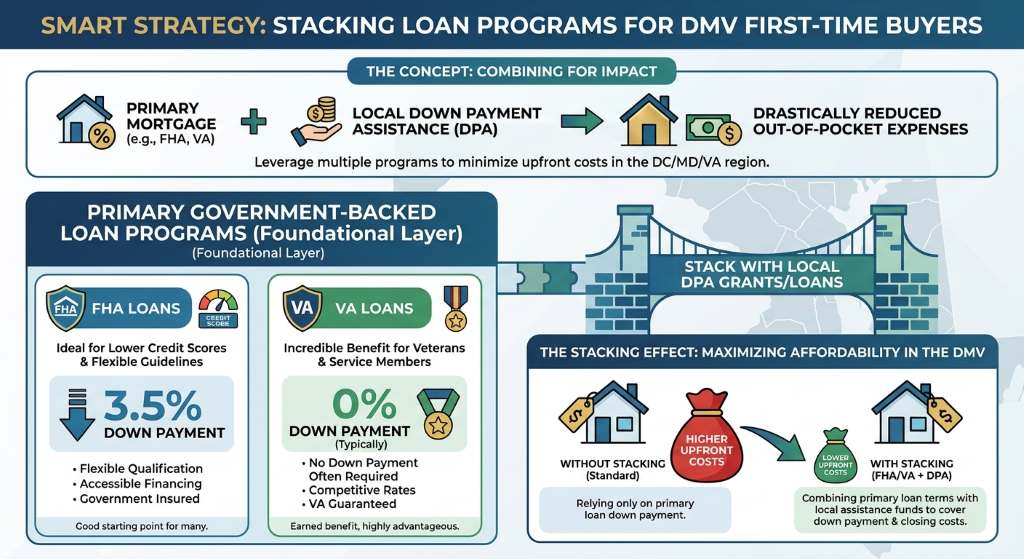

Stacking Mortgage Programs and Down Payment Assistance

One of the most effective strategies for first-time homebuyers in the DMV is stacking loan programs. This means combining a primary mortgage with local down payment assistance (DPA) to drastically reduce your out-of-pocket expenses.

Here is a closer look at the primary government-backed loan programs available:

- FHA Loans: Ideal for buyers with lower credit scores. These require just a 3.5% down payment and offer flexible qualification guidelines.

- VA Loans: An incredible benefit for veterans and active-duty military personnel, offering zero down payment and no private mortgage insurance requirements.

- USDA Loans: Perfect for buyers looking at designated rural or suburban areas in Maryland and Virginia, providing 100% financing for eligible properties.

To maximize your buying power, you can pair these mortgages with local state initiatives. Programs like DC Open Doors, the Maryland Mortgage Program (MMP), and Virginia Housing (VHDA) offer grants or deferred loans that cover down payments and closing costs. Stacking these benefits allows you to keep more cash in your savings account while securing a highly competitive interest rate.

| Loan Program | Minimum Down Payment | Typical Credit Score Needed | Best For |

|---|---|---|---|

| FHA Loan | 3.5% | 580+ | Buyers needing flexible credit guidelines |

| VA Loan | 0% | No strict minimum | Veterans and active military personnel |

| USDA Loan | 0% | 640+ | Buyers in designated rural or suburban areas |

| Conventional | 3% | 620+ | Buyers with strong credit and stable income |

Tactical Advice for Competing in the DMV

In a high-cost area like the DMV, preparation is your greatest asset. Sellers want assurance that your financing is solid and that the transaction will close smoothly and on time. Partnering with an independent broker gives you access to multiple lenders, ensuring you find the best rates and terms without being locked into a single bank’s limited offerings.

Here are a few tactical steps to strengthen your offer and stand out to sellers:

- Secure a fully underwritten pre-approval: This shows sellers you are a serious buyer with guaranteed funding, making your offer nearly as strong as cash.

- Be flexible but firm: Know your budget limits and stick to them, but remain open to negotiating closing timelines or minor repair contingencies.

- Leverage your broker’s network: The Mortgage Know team works closely with local real estate agents to ensure your offer is presented professionally and competitively.

Remember, buying a home is a marathon, not a sprint. With clear communication and transparent loan options, we take the stress out of the mortgage process so you can focus entirely on finding the perfect home.

Q1: What is the minimum down payment for a first-time homebuyer in the DMV?

Depending on the loan program, you can buy a home with as little as 0% down using a VA or USDA loan, or 3.5% down with an FHA loan. Local down payment assistance programs can also help cover these initial costs.

Q2: Can I combine a VA loan with a Maryland or Virginia down payment assistance program?

Yes. Many local housing finance agencies allow you to stack their down payment and closing cost assistance grants with VA, FHA, or conventional loans to minimize your out-of-pocket expenses.

Q3: How do I know if I qualify for DC Open Doors?

DC Open Doors is available to both first-time and repeat homebuyers purchasing a home in Washington DC. Qualification is based on your income, credit score, and the maximum loan limits, which an independent mortgage broker can easily help you navigate.

Q4: Why should I use an independent mortgage broker instead of my local bank?

An independent broker like Richard Jones works for you, not the bank. This gives you access to a wider variety of loan products, more competitive interest rates, and personalized advice tailored to your specific financial situation.

Q5: Does a low credit score disqualify me from buying a home in Maryland or Virginia?

Not necessarily. FHA loans are designed with flexible credit guidelines, often accepting scores as low as 580. We can review your financial profile and help you explore the best path to achieving homeownership.Schedule Your Free Mortgage Consultation Today